We value Amazon at over $700 per share. Our analysis assumes Amazon’s is able to continue to aggressively grow its big three (i.e. Marketplace, Prime and Amazon Web Services) for the next five years before finally slowing up on innovation and growth, and instead focusing more on bottom line results. Of course this is contrary to Amazon’s 18+ year history as a public company whereby they’ve focused relentlessly on innovation instead of the bottom line. But before getting into the details of our valuation, the following quote from Amazon’s 1997 Letter to Shareholders provides important color as to Amazon’s priorities, and it is a quote Amazon founder and CEO, Jeff Bezos, continues to stand by today (he included it in his 2014 Letter to Shareholders too):

“We will continue to make investment decisions in light of long-term market leadership considerations rather than short-term profitability considerations or short-term Wall Street reactions.”

Amazon’s Earning History:

True to Bezo’s quote, Amazon’s earnings history demonstrates a clear prioritization of long-term growth over short-term profits. Amazon has generated almost a quarter trillion (with a “t”) dollars in revenue over the last three calendar years, but it has still managed to have negative net income in two of the last three years and negative net income in aggregate over the three year period (2014 Annual Report, p.17). To some extent, the negative net income is due to thin margins in the retail sales business (margins are higher in Amazon Web Services (AWS), but this is currently a much smaller business). However, a bigger reason for the negative net income is the enormous amount of spending on innovation and growth. For example, Amazon spent over $9 billion on research and development (R&D) in 2014, and the company could have easily generated significantly positive net income simply by cutting back on its R&D spending. However, spending on R&D, innovation and risky long-term growth opportunities is in Amazon’s DNA; it’s the reason value investors hate Amazon, and growth investors love it.

Amazon’s Growth Opportunities:

Jeff Bezos concludes the body of his most recent Annual Letter to Shareholders as follows:

“Marketplace, Prime, and Amazon Web Services are three big ideas. We’re lucky to have them, and we’re determined to improve and nurture them – make them even better for customers. You can also count on us to work hard to find a fourth. We’ve already got a number of candidates in work, and as we promised some twenty years ago, we’ll continue to make bold bets. With the opportunities unfolding in front of us to serve customers better through invention, we assure you we won’t stop trying.”

The quote indicates that Amazon clearly intends to continue its bold pursuit of growth and innovation, both within the big three and beyond. For reference:

Marketplace is Amazon.com's fixed-price online marketplace that allows sellers to offer new and used items alongside Amazon's regular offerings.

Prime is Amazon’s $99 annual membership service that offers a variety of benefits including free expedited shipping, instant video streaming of movies and TV episodes, music, and books, to name a few.

Amazon Web Services (AWS) is a collection of remote computing services that make up a cloud-computing platform offered by Amazon.com.

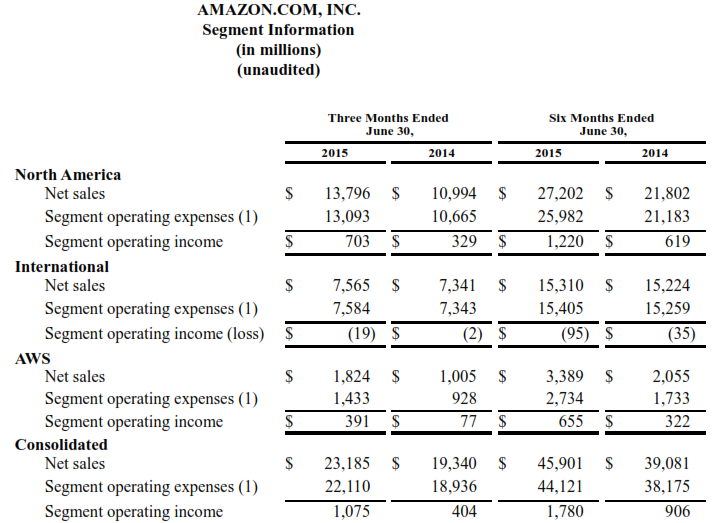

With regard to these three big ideas, Marketplace and Prime have been the major drivers of Amazon’s roughly 20% annual revenue growth over the last several years (mainly because they are much larger businesses). However, this is changing quickly. AWS has a much higher revenue growth rate and a much higher operating margin than the other two, and Amazon recently began including AWS in its segment breakout information:

As AWS continues to grow at a faster pace (and with higher margins) than Marketplace and Prime, it is increasingly becoming a more meaningful driver of value creation for Amazon. Amazon’s second quarter press release highlights some specific examples of AWS expansion including:

The opening of a new AWS region in India in 2016, which will enable customers to run workloads in India and serve Indian end-users with even better latency.

The launch of 350 significant AWS features and services year-to-date (ahead of last year’s pace).

The release of AWS Educate, a free program that helps educators and students use real-world cloud technology in the classroom to prepare students for the cloud workforce.

The construction and operation of Amazon Solar Farm U.S. East and Amazon Wind Farm U.S. East to generate approximately 170,000 megawatt hours (MWh) of solar power and 670,000 MWh of wind energy on an annual basis to be delivered into the electrical grids that power both current and future AWS data centers.

The release of AWS Device Farm, a new service that helps mobile app developers quickly and securely test their apps on smartphones, tablets, and other devices to improve the quality of their Android and Fire OS apps.

With regards to the North America and International segments (see table above), North America has been growing at a faster pace, and Amazon Prime has been a big driver of this growth. An RBC Capital Markets survey suggests about 40% of Amazon customers are Prime members today, up from about 25% in 2013. The survey also suggest there may be as many as 50 million Prime members in the US, and as many as 60 to 80 million globally, up from an estimated 30 – 40 million and 50 million, respectively, a year ago. And the survey not only indicates that customers are willing to pay for Prime, but that Prime members spend more money too.

And while North America has been growing at a faster pace, there are clearly opportunities to increase International growth. Amazon highlights some of its International growth initiatives in its second quarter press release including the expansion of Prime Now one-hour delivery in London, and expansion of the Fire HD Kids Edition tablet to the UK and Germany, for example. Additionally, there are opportunities to expand International Prime memberships (and overall business) to a level closer to that of North America.

Valuing Amazon:

We use a discounted cash flow model to value Amazon at $712 per share. We assume the company will continue to grow at a fast-pace over the next five years based on the opportunities presented by Marketplace, Prime and AWS; and after five years we assume the company’s growth rate will level off but it will also benefit from a reduction in R&D spending. More specifically, we assume Amazon can grow its cash flow from operations by 22% per year for the next five years before reverting to a more market-normal growth rate of 2.5% (we use 22% as a conservative estimate; it’s less than the growth rate in 2013 and 2014, and significantly less than the trajectory through the first half of 2015, see investor presentation). We also assumed the company will increase its capital expenditures to $6 billion in each of the next five years, and then increase capex by 2.5% per year thereafter. For reference, cash capex was only $4.9 billion, $3.4 billion, $3.8 billion and $1.8 billion in 2014, 2013, 2012 and 2011, respectively (Annual Report, p.22). We use a required rate of return of 8.3% (WACC, CAPM).

One of the biggest assumptions in our valuation is that Amazon will dramatically slow its rate of innovation and capex spending after AWS has finished “ramping up” in five years. This is contrary to Amazon’s “never stop inventing” attitude, but it is a conservative way to value the company. And if Amazon continues to grow aggressively after five years then the stock is worth even more than our valuation suggests. On the other hand, if Amazon is not successful, and the company never gets out of this negative net income stage of its latest j-curve, then the company is just destroying value, and stockholders would be well-served to sell now.

There are a myriad of other scenarios that could play out for Amazon, and this is part of the reason the stock price is so volatile. For example, Amazon could spin off its high margin AWS business leaving current stockholders with shares of two separate companies (the low margin marketplace/prime business and the high margin AWS business). Or, Amazon may figure out how to reduce costs, increase margins, and dramatically increase its stock price by using drones, for example, to efficiently deliver orders (Amazon Prime Air).

Or, as Jeff Bezos hopes, Amazon may invent a fourth big idea which could dramatically change the valuation altogether. The possibilities are endless, and this is a big contributor to Amazon’s stock price volatility.

Risks:

There are a variety of risk factors that could negatively impact Amazon. For example, cloud competition could deprive AWS of future market share. Thus far, it seems AWS may be finding a niche with smaller and newer companies, but Microsoft, for example, has a strong foothold at the larger enterprise level, and could prevent AWS from achieving large scale growth. Microsoft conveniently points out some of their advantages over AWS here: Microsoft Azure vs. Amazon Web Services (AWS). And Microsoft is only one source of completion. Others include IBM, Google and Salesforce.

Another risk is that Amazon could simply overspend on research and development without ever achieving significant profitability. This has been a common complaint from value investors as the company continues to generate very little profit relative to its massive revenues. Amazon recently increased its debt to help fund growth opportunities (not necessarily a bad idea in this low interest rate environment). Specifically, long-term debt has grown from $255 million in 2011 to $8.25 billion as of June 30, 2015 (and it was as high as $9.9 billion at the end of 2014).

Another risk is that Amazon’s management could start making bad decisions on how it spends its free cash flow. For example, if Amazon isn’t able to grow organically then management could start destroying shareholder value with bad acquisitions. Amazon highlights this risk nicely on pages 9 and 10 of its most recent annual report giving specific examples of how their “business could suffer if we are unsuccessful in making, integrating and maintaining acquisitions and investments.” Amazon has demonstrated a propensity to make significant acquisitions (for example Amazon paid $842 million in cash for Twitch in 2014, $1.2 billion for Zappos in 2009, and an estimated 0.33 to 0.5 billion for Elemental Technologies in 2015). Interestingly, the majority of Amazon’s voting rights are not owned by insiders (there is only one class of stock, and CEO Jeff Bezos (and other directors) only own 18.2%). Therefore, there could be significant activist pressure on Amazon to start focusing on the bottom line and returning cash to shareholders through buybacks and dividends if the company’s revenue growth rate slows down significantly within the next few years.

Conclusion:

Amazon is risky and volatile, but there is a feasible growth path that makes it worth significantly more than its already enormous $250 billion market capitalization. Following its current wave of growth initiatives, if Amazon were unable to identify additional growth opportunities then the company would likely have more than enough cash to return to shareholders (via dividends and share repurchases) to make it worth $700+ per share. However, for the foreseeable future (and to the chagrin of many value investors), Amazon will continue to focus more on growth than on profitability.